Target Corporation (TGT), a leading retail giant in the United States, stands as a testament to retail excellence and strategic growth. With its headquarters in Minneapolis, Minnesota, Target has carved out a significant niche in the retail sector by offering customers a wide array of products, including essentials, home goods, electronics, and apparel, through both its expansive network of stores and robust online platform. Target’s commitment to combining quality with value, along with its focus on creating a seamless shopping experience, has solidified its position as a favorite among consumers.

Remarkably, Target has demonstrated not just resilience but also a strong commitment to its shareholders, as evidenced by its remarkable track record of increasing its dividend for 55 consecutive years. This achievement places Target in the esteemed group of Dividend Kings, a select group of companies known for their exceptional dividend growth history. This unwavering commitment to returning value to shareholders, even amidst the ever-evolving retail landscape, underscores Target’s financial health and strategic foresight, making it a noteworthy entity in the retail sector and an attractive proposition for investors looking for stable, long-term returns.

Analyst Ratings

- Kate McShane from Goldman Sachs maintains a “Strong Buy” rating on the stock as of Feb 1, 2024, with no price target provided.

- Simeon Gutman from Morgan Stanley upgrades the stock from “Hold” to “Buy” with a price target increase from $140 to $165, indicating a +14.24% upside, on Jan 16, 2024.

- George Kelly of Wells Fargo maintains a “Buy” rating, adjusting the price target from $148 to $155, reflecting a +7.32% upside, as of Jan 4, 2024.

- Bill Kirk at Roth MKM reiterates a “Hold” rating with a $140 price target, suggesting a -3.07% downside, on Nov 16, 2023.

- Paul Lejuez from Citigroup maintains a “Hold” rating, raising the price target from $117 to $142, which implies a -1.68% downside, on Nov 16, 2023.

- Mark Astrachan of Stifel maintains a “Hold” rating, with the price target increased from $130 to $141, indicating a -2.37% downside, on Nov 16, 2023.

- Kelly Bania from BMO Capital maintains a “Hold” rating, updating the price target from $120 to $130, showing a -9.99% downside, on Nov 16, 2023.

- Steven Shemesh at RBC Capital maintains a “Buy” rating, with a price target adjustment from $161 to $157, suggesting a +8.70% upside, on Nov 16, 2023.

- Christopher Horvers of JP Morgan maintains a “Hold” rating, with the price target increased from $113 to $125, indicating a -13.45% downside, on Nov 16, 2023.

Insider Trading

Over the last 6-12 months, insiders at the company have engaged in various buy and sell transactions, showcasing a mix of strategic dispositions and post-exercise sales, reflecting active management of their holdings in the company’s stock. Notably, the transactions provide insights into the insiders’ confidence and financial planning strategies regarding their stock ownership.

Matthew L Zabel, a Corporate Affairs executive, engaged in multiple sell transactions, including a notable sale post-exercise on January 29, 2024, of 163 shares at $139.66 each and another direct sell on November 28, 2023, disposing of 4,000 shares at $131.33 each. This activity suggests a pattern of capitalizing on stock options, potentially to diversify personal investment portfolios or realize gains. Similarly, Christina Hennington, an EVP, sold 4,000 shares on November 22, 2023, at $130.55, and Don H Liu, a Division Officer, conducted a significant sale of 16,000 shares at $130.00 on November 16, 2023. Brian C Cornell, the Chair & CEO, also made a substantial sale post-exercise on August 18, 2023, offloading 30,000 shares at $130.70.

These transactions, particularly the sales following option exercises, suggest that insiders are taking advantage of the stock’s valuation to secure profits, a common practice among corporate executives. However, such sales should not automatically be seen as a lack of confidence in the company’s future prospects but rather as part of personal financial management strategies. The activity of insiders, especially in a company like this with a significant history of dividend increases, remains a point of interest for investors interpreting the long-term value and stability of their investments.

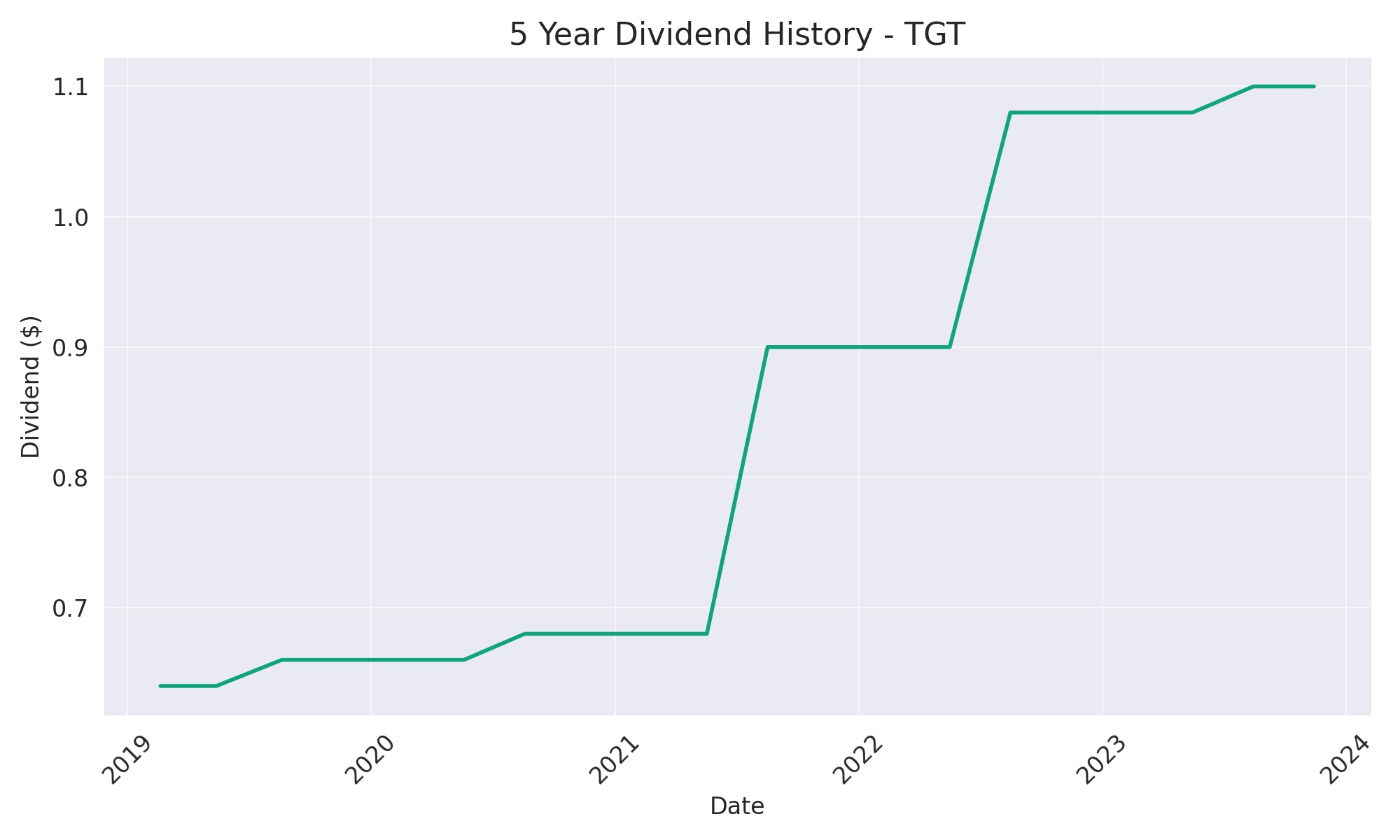

Dividend Metrics

Target Corporation (TGT), a key player in the retail sector, has shown a dedication to its shareholders with a distinguished history of increasing dividends for 55 years straight. The current dividend yield stands at 3.13%, which is notably higher than the five-year average yield of 2.27%. This suggests that shareholders have been receiving a gradually more generous share of profits, underscored by a five-year dividend growth rate of 8.45%. Despite this positive trend in shareholder returns, the company has experienced a slight contraction in revenue, with a one-year revenue growth percentage at -4.20%.

The payout ratio, which indicates the proportion of earnings distributed as dividends, is maintained at 55%, reflecting a balanced approach between returning income to shareholders and reinvesting in the company. However, the stock has faced headwinds over the past year, with a one-year return percentage of -20.65%, signaling that despite the company’s robust dividend record, investors have seen a notable dip in the stock’s market value during this period. This juxtaposition of strong dividend performance against a challenging market return highlights the dual facets of investor consideration: income and capital appreciation.

Dividend Value

Target Corporation (TGT) presents an intriguing case for value analysis when its current dividend yield is stacked against its five-year average. The current yield of 3.13% towers over the five-year average of 2.27%, suggesting that the stock might be undervalued if we consider the dividend yield as a marker of investor returns. This disparity between the present yield and the historical average could signal that Target’s stock is currently offering a higher income return for investors compared to the recent past, which might attract dividend investors who are on the hunt for stocks with the potential for both income and capital appreciation.

The elevated yield could be partially attributed to market reactions to short-term challenges or possibly investor skepticism about future growth prospects, which has pressured the stock price and, consequently, bloated the yield. However, if the company’s fundamentals remain strong, the higher yield might represent a temporary sale in the equity market aisle, potentially ripe for investors who have faith in the company’s long-term story. Such a condition could be particularly enticing in a historically low-interest-rate environment, where income-generating investments are highly sought after.

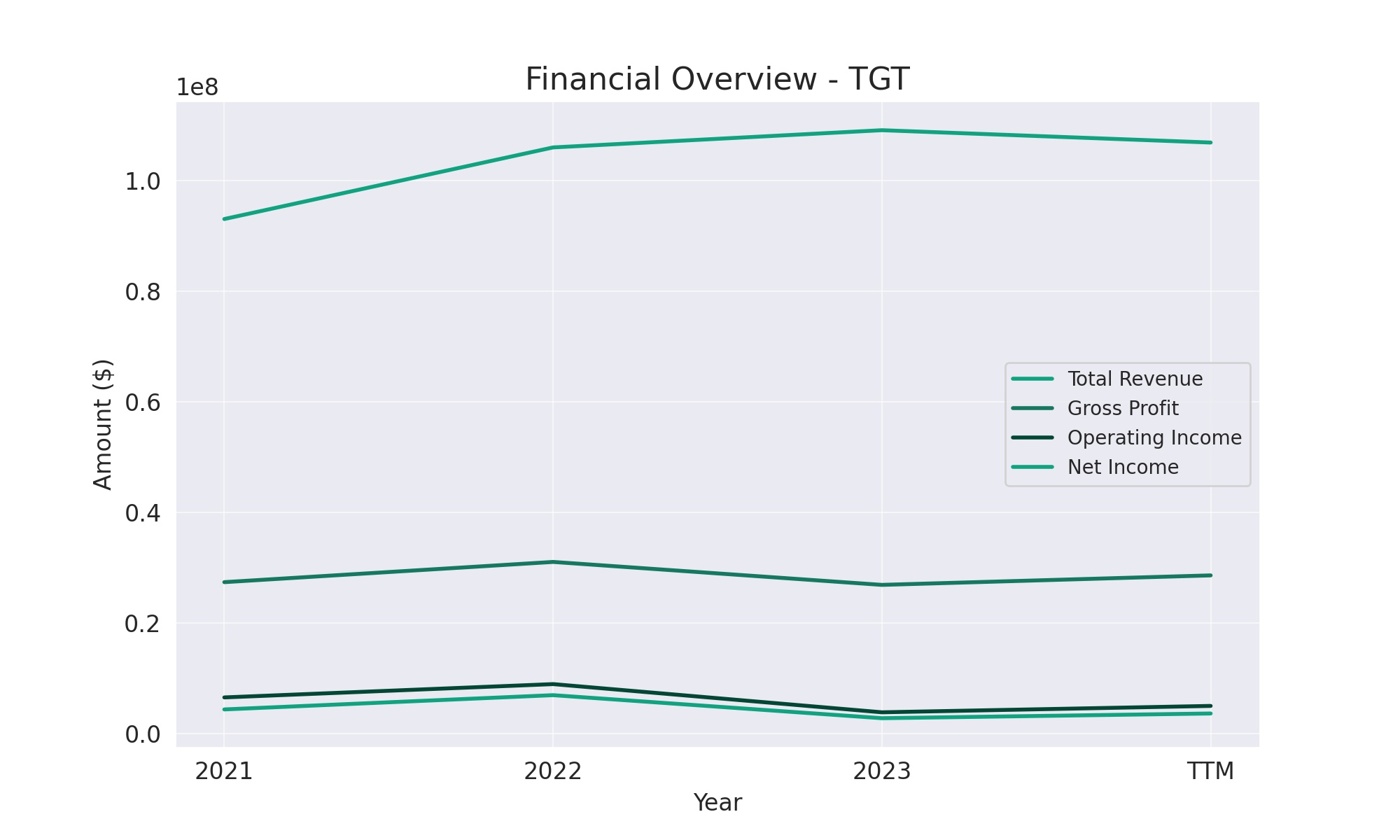

Income statement Analysis

In the latest financial saga of our protagonist, the stock, it navigated the choppy seas of market demands to report a total revenue of $106,888,000 in the TTM, slightly down from the $109,120,000 crest of the previous fiscal wave. The cost of revenue, akin to the price of admission to the grand revenue theater, was tallied at $78,279,000, which leaves one to ponder whether the cost of the show is inching closer to the price of the tickets sold. Meanwhile, the gross profit, which serves as the company’s financial applause, dimmed to $28,609,000 from a more thunderous applause of $31,042,000, suggesting the audience may be a tad less enthusiastic.

The operating income, a key performance encore, took a bow at $5,001,000 in the TTM, which, while commendable, couldn’t quite match the previous year’s standing ovation of $8,946,000. On the tax stage, the provision was a more modest $922,000, down from the $1,961,000 tax act in the spotlight two years ago. Net income, the final curtain call, presented a tale of two cities: a prosperous $6,946,000 metropolis followed by a more humble $3,632,000 village. Such figures could prompt investors to wonder if this is merely an intermission in profits or if the company’s fiscal performance is setting the stage for a different genre altogether.

Balance sheet Analysis

For Target Corporation (TGT), the balance sheet as of January 31, 2023, reveals a slight shrinkage in the total assets, from $53,811,000 the year prior to $53,335,000. This marginal dip, resembling a shopper who decides against the extra pack of gum at checkout, suggests a cautious approach in asset accumulation or a subtle shift in asset values. Meanwhile, the total liabilities net minority interest have swelled up like a balloon at a birthday party, from $36,808,000 to $42,103,000, perhaps indicating that TGT has been filling its financial obligations with a bit more air than usual.

The equity side of the ledger shows that shareholders’ slice of the pie has been nibbled down from $14,440,000 to $11,232,000, a trend that might leave equity gourmands feeling a tad peckish. The working capital, too, has taken a turn into the negatives, sitting at -$1,654,000, which in layman’s terms, could be compared to digging into the couch cushions for extra change. Despite this, TGT’s capital lease obligations and net debt figures have been managed with the precision of a price gun, displaying a level of control over long-term commitments. In the retail giant’s financial storefront, the display suggests cautious asset management amid a dynamic fiscal environment.

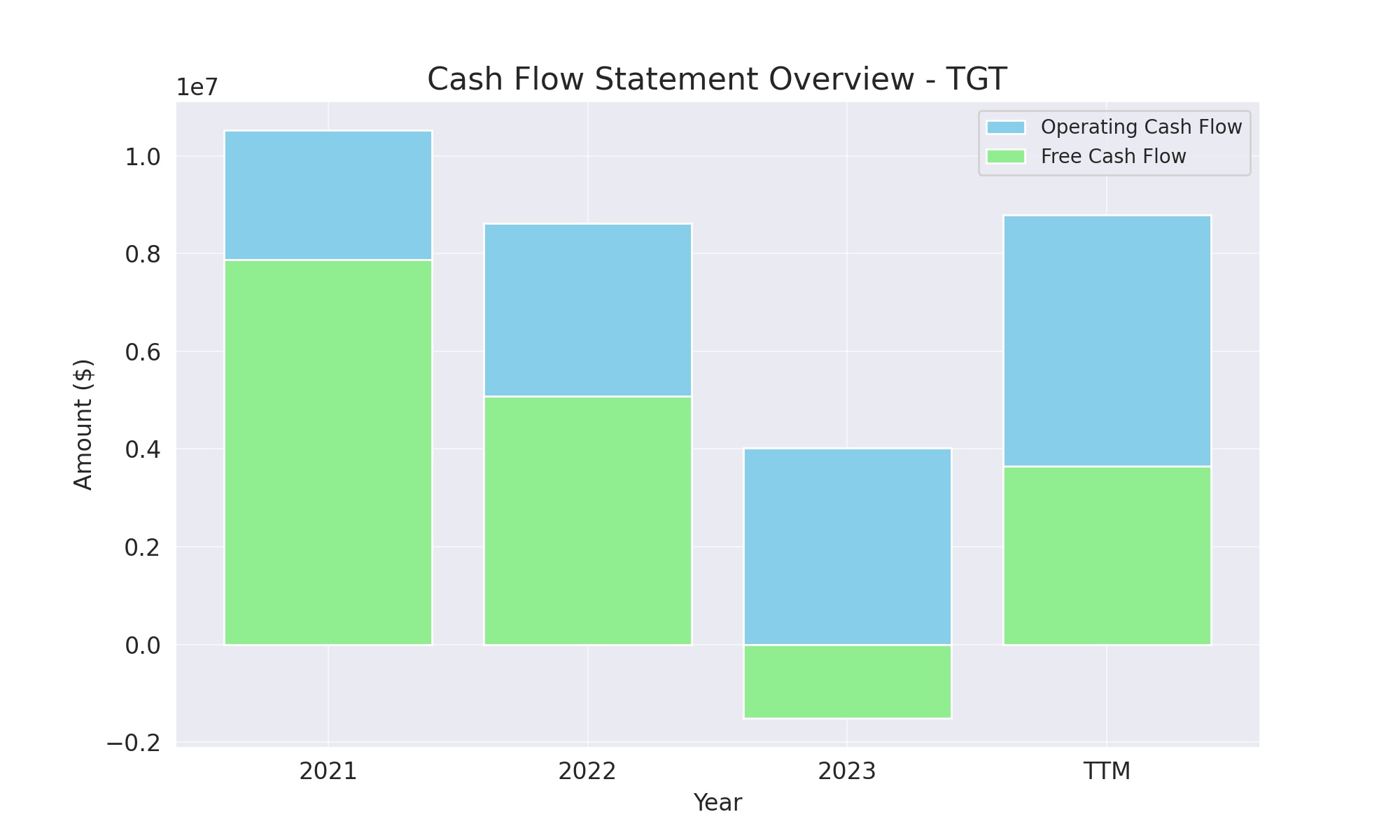

Cash Flow Statement Analysis

Target Corporation’s cash flow narrative over the trailing twelve months has been akin to a carefully choreographed retail dance rather than an unpredictable thriller. The operating cash flow pirouetted to $8,798,000, a lively leap from the more modest $4,018,000 observed the year before. This robust performance suggests that TGT’s operational cash register has been ringing more merrily, offering a melody of financial fluidity that is music to an investor’s ears.

However, the investing cash flow has taken a decisive step in the opposite direction, recording an outflow of $5,111,000, as if the company has been on a bit of a spending spree, albeit a strategic one, likely investing in long-term growth projects. The financing cash flow, which reflects the company’s financial maneuvers, also saw money marching out the door to the tune of $2,731,000. Despite this, the end cash position, which is the final note in this fiscal symphony, holds a modest $1,910,000. It may not be a standing ovation-worthy finale, but it does indicate that TGT is keeping its financial stage managed and ready for the next act.

SWOT Analysis

Target Corporation (TGT), a leading player in the retail industry, presents a distinct profile when assessed through a SWOT analysis:

Strengths:

- Brand Recognition: TGT boasts strong brand recognition and a loyal customer base, thanks to its reputation for style, quality, and value.

- Diversified Product Mix: Offering everything from groceries to clothing and electronics, TGT attracts a wide demographic, helping to stabilize sales across economic cycles.

- Supply Chain Efficiency: TGT has invested heavily in its supply chain, making it more agile and resilient – an advantage in meeting consumer demand quickly and efficiently.

Weaknesses:

- Thin Profit Margins: As with many retailers, TGT operates on relatively thin profit margins, which can be squeezed by factors like wage increases and supply chain disruptions.

- Physical Store Footprint: While TGT has a strong physical presence, this can also be a liability in terms of overheads and flexibility compared to online-only competitors.

Opportunities:

- E-Commerce Expansion: Continued growth in online sales and omnichannel retailing presents TGT with opportunities to capture market share from competitors who are slower to adapt.

- Private Labels: TGT’s private label brands are well-regarded and offer higher margins than name-brand products, providing a potential growth area.

- Global Expansion: While TGT is a leader in the U.S., there’s potential for international expansion, which could open up new markets and revenue streams.

Threats:

- Competitive Market: TGT faces stiff competition from both brick-and-mortar rivals and e-commerce giants like Amazon, which can impact market share and pricing power.

- Economic Downturns: Economic contractions can lead to reduced consumer spending, particularly on the non-essential goods that make up a significant portion of TGT’s sales.

- Cybersecurity Risks: As TGT continues to grow its online presence, it must manage the risks associated with data security and privacy in an increasingly digital landscape.

In conclusion, TGT’s strong brand and market presence, diversified offerings, and efficient supply chain position it well in the competitive retail landscape, but it must navigate challenges such as tight profit margins, heavy competition, and the risks associated with an evolving retail environment.

Competitors

Target Corporation (TGT) competes with a mix of brick-and-mortar and online retailers, each presenting unique strengths within the retail landscape:

- Walmart Inc. (WMT): The world’s largest retailer, Walmart, offers a broad assortment of goods at low prices, with a significant physical presence and growing e-commerce platform, challenging TGT in both price and scale.

- Amazon.com Inc. (AMZN): As the leading e-commerce platform, Amazon competes aggressively with TGT in the online retail space, offering a wide range of products, including groceries through its Whole Foods Market subsidiary.

- Costco Wholesale Corporation (COST): Specializing in membership-based warehouse clubs, Costco attracts customers with its bulk purchasing options and competitive pricing, competing with TGT on value for money.

- The Home Depot, Inc. (HD): As the largest home improvement retailer, Home Depot competes with TGT in the home goods and appliances sector, appealing to DIYers and professional contractors.

- Kroger Co. (KR): One of the largest supermarket chains in the U.S., Kroger competes with TGT’s grocery segment, offering a wide variety of food and household products at competitive prices.